Interactive Brokers (IB) API Example Using IBAPI - Part 2

July 12, 2019

Introduction

Last blog I showed how to set up Interactive Brokers (IB) API (IBAPI) using Python 3.6. My desire was to create stock price graphs for the US market using the SPY ETF. I added momentum indicators to the graphs showing positive or negative periods of momentum.

I will go through the Interactive Brokers Application Programming Interface (IBAPI) code on Windows.

Links

I used the following links to assist with setting up the Interactive Brokers API.

-

The API itself can be downloaded and installed from: interactivebrokers.github.io.

-

The other required software is the [IB Gateway for Windows] (https://www.interactivebrokers.ca/en/index.php?f=16457 “IB Gateway for Windows”). This software runs continuously on your computer and listens for API calls which it executes on the IB trading system, creating actual trades.

-

Python3 [Python3] (https://www.python.org/downloads/windows/ “Python3”).

-

I use the free Visual Studio Code IDE because of its built-in debugger [Visual Studio Code IDE] (https://code.visualstudio.com/ “Visual Studio Code IDE”).

Visual Studio Code

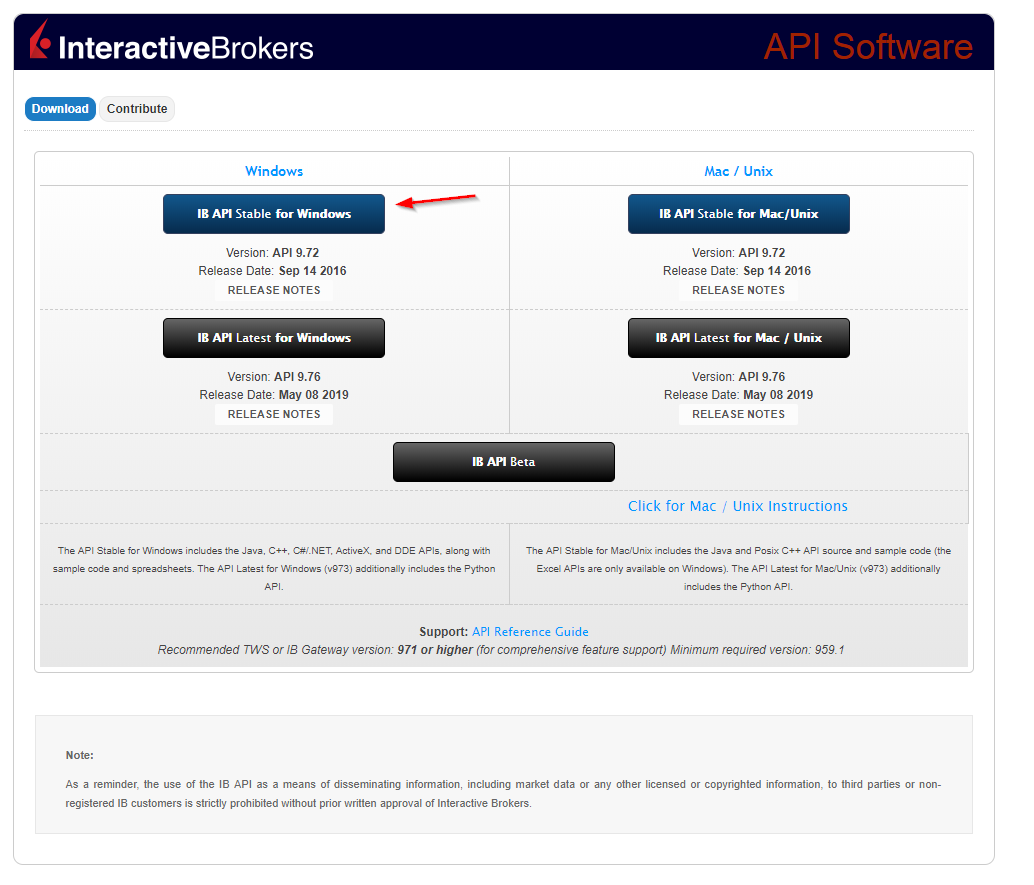

Follow the link to download the API code to your local drive interactivebrokers.github.io.

-

Select the stable version.

-

Install the .msi file (TWS API Install 972.18.msi), this will create a folder on your C drive C:\TWS API

-

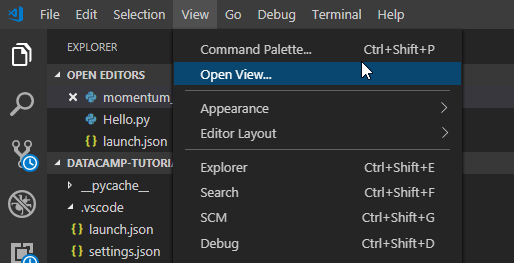

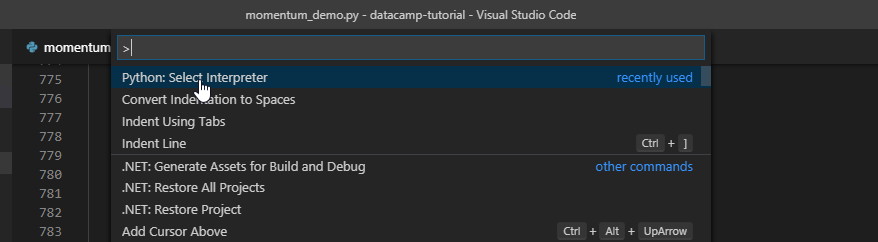

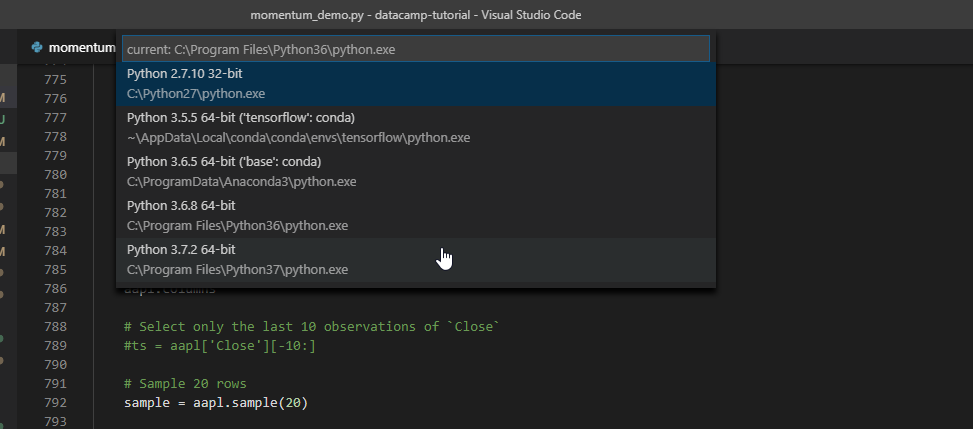

Open Visual Studio Code and open the command palette and select the python interpreter, choose Python36.

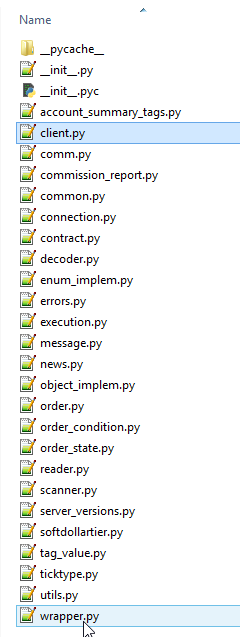

IBAPI Folder and Files

The folder of interest is called ibapi. Within this folder there are key files used in your application.

- ibapi/wrapper.py Provides the core functionality and used in your main application class

- ibapi/client.py Is the ibapi client which is initialized first in your application. The client communicates with the API and contains the connect() function.

I also used two important files in the Testbed folder: ContractSamples.py and OrderSamples.py Both of these files will allow you to create orders using the client placeOneOrder() function

- Find the Testbed folder and place it in your project directory. I put the folder in my project root. You should have ibapi and Testbed folders.

Include Files

Now we will again include the files into our main application Python file. The important includes are as follows

import ibapi.wrapper from ibapi.client import EClient from Testbed.ContractSamples import ContractSamples from Testbed.OrderSamples import OrderSamples

from ibapi.wrapper import EWrapper

import ibapi.decoder

import ibapi.wrapper

from ibapi.common import *

from ibapi.ticktype import TickType, TickTypeEnum

from ibapi.comm import *

from ibapi.message import IN, OUT

from ibapi.client import EClient

from ibapi.connection import Connection

from ibapi.reader import EReader

from ibapi.utils import *

from ibapi.execution import ExecutionFilter

from ibapi.scanner import ScannerSubscription

from ibapi.order_condition import *

from ibapi.contract import *

from ibapi.order import *

from ibapi.order_state import *

from Testbed.ContractSamples import ContractSamples

from Testbed.OrderSamples import OrderSamples

Your imports/includes could end up looking very long. I have the following as my imports for my entire trading algorithm.

import sys

import socket

import struct

import array

import inspect

import time

import argparse

import os.path

import json

import csv

from pprint import pprint

import twitter

from fred import Fred

import smtplib

from email.mime.text import MIMEText

from email.mime.image import MIMEImage

from email.mime.application import MIMEApplication

from email.mime.multipart import MIMEMultipart

from email.header import Header

from email.utils import formataddr

import urllib

#import urllib2

import requests

from bs4 import BeautifulSoup as bs

import shutil

from ibapi.wrapper import EWrapper

import ibapi.decoder

import ibapi.wrapper

from ibapi.common import *

from ibapi.ticktype import TickType, TickTypeEnum

from ibapi.comm import *

from ibapi.message import IN, OUT

from ibapi.client import EClient

from ibapi.connection import Connection

from ibapi.reader import EReader

from ibapi.utils import *

from ibapi.execution import ExecutionFilter

from ibapi.scanner import ScannerSubscription

from ibapi.order_condition import *

from ibapi.contract import *

from ibapi.order import *

from ibapi.order_state import *

from Testbed.ContractSamples import ContractSamples

from Testbed.OrderSamples import OrderSamples

import datetime

import datetime as dt

from datetime import timedelta

import quandl as qdl

# Install https://www.anaconda.com/download/

import pandas_datareader as pdr

import pandas as pd

# Import Matplotlib's `pyplot` module as `plt`

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

import numpy as np

import matplotlib.dates as mdates

import matplotlib.cbook as cbook

#import statsmodels.api as sm

# Import the `datetools` module from `pandas`

#from pandas.core import datetools

import pandas.tseries as pdts

Program File

Now we are ready to create our program. After the includes, lets create the TestApp class including the Client and Wrapper classes. We will try to place a test order.

- Create a placeOneOrder function

- Use OrderSamples to create a BUY order for 100 shares

- Select the account, in this case account DU9000000 Remember: do not connect to your live account, but instead use your paper account.

- call the Client function placeOrder with a sample USStock. The ContractSamples.USStock() returns a test stock.

- That’s it! you created a Market Order for a stock!

# Script only works with python 3.6 (view > command palette > python: Select Interpreter > select 3.6)

class TestApp(EClient, EWrapper):

def __init__(self):

EClient.__init__(self, self)

self.nextValidOrderId = 10

@iswrapper

def nextValidId(self, orderId:int):

super().nextValidId(orderId)

logging.debug("setting nextValidOrderId: %d", orderId)

self.nextValidOrderId = orderId

def placeOneOrder(self):

#self.simplePlaceOid = self.nextOrderId()

faOrderOneAccount = OrderSamples.MarketOrder("BUY", 100)

faOrderOneAccount.account = "DU9000000"

self.placeOrder(self.nextOrderId(), ContractSamples.USStock(), faOrderOneAccount)

def main():

#put your calls in here

if __name__ == "__main__":

main()

We can continue adding a few more wrapper functions to get order information such as order status. Add some more variables in the init function.

# Script only works with python 3.6 (view > command palette > python: Select Interpreter > select 3.6)

class TestApp(EClient, EWrapper):

def __init__(self):

EClient.__init__(self, self)

self.nextValidOrderId = 10

self.simplePlaceOid = None

self.permId2ord = {}

self.hData = {}

self.hDataColumns = ['Date','Open','High','Low','Close','Volume','BarCount','Average']

self.hDataIndex = []

self.hDataRecords = []

self.lineCount = 0

self.hDataCurrent = False

self.hDataMonthly = False

self.cDataPrice = 0

self.currentSymbol = "SPY"

@iswrapper

def nextValidId(self, orderId:int):

super().nextValidId(orderId)

logging.debug("setting nextValidOrderId: %d", orderId)

self.nextValidOrderId = orderId

def placeOneOrder(self):

#self.simplePlaceOid = self.nextOrderId()

faOrderOneAccount = OrderSamples.MarketOrder("BUY", 100)

faOrderOneAccount.account = "DU9000000"

self.placeOrder(self.nextOrderId(), ContractSamples.USStock(), faOrderOneAccount)

def getWebFile(self, URL, fileName):

headers = {'User-Agent': 'Mozilla/5.0 (Macintosh; Intel Mac OS X 10_11_5) AppleWebKit/537.36 (KHTML, like Gecko) Chrome/50.0.2661.102 Safari/537.36'}

local_filename = fileName

pdf_request = requests.get(URL + local_filename, headers=headers, stream=True)

with open('data/' + local_filename, 'wb') as f:

shutil.copyfileobj(pdf_request.raw, f)

@iswrapper

def error(self, *args):

super().error(*args)

print(current_fn_name(), vars())

@iswrapper

def winError(self, *args):

super().error(*args)

print(current_fn_name(), vars())

@iswrapper

def openOrder(self, orderId:OrderId, contract:Contract, order:Order,

orderState:OrderState):

super().openOrder(orderId, contract, order, orderState)

print(current_fn_name(), vars())

order.contract = contract

self.permId2ord[order.permId] = order

@iswrapper

def openOrderEnd(self, *args):

super().openOrderEnd()

logging.debug("Received %d openOrders", len(self.permId2ord))

@iswrapper

def orderStatus(self, orderId:OrderId , status:str, filled:float,

remaining:float, avgFillPrice:float, permId:int,

parentId:int, lastFillPrice:float, clientId:int,

whyHeld:str):

super().orderStatus(orderId, status, filled, remaining,

avgFillPrice, permId, parentId, lastFillPrice, clientId, whyHeld)

@iswrapper

def tickPrice(self, tickerId: TickerId , tickType: TickType, price: float, attrib):

super().tickPrice(tickerId, tickType, price, attrib)

print(current_fn_name(), tickerId, TickTypeEnum.to_str(tickType), price, attrib, file=sys.stderr)

#tickPrice 1001 LAST 264.42 0,0

if(TickTypeEnum.to_str(tickType) == 'LAST'):

self.cDataPrice = price

@iswrapper

def tickSize(self, tickerId: TickerId, tickType: TickType, size: int):

super().tickSize(tickerId, tickType, size)

print(current_fn_name(), tickerId, TickTypeEnum.to_str(tickType), size, file=sys.stderr)

@iswrapper

def tickSnapshotEnd(self, reqId: int):

super().tickSnapshotEnd(reqId)

print("TickSnapshotEnd:", reqId)

if(self.isConnected()):

self.disconnect()

@iswrapper

def realtimeBar(self, reqId:TickerId, time:int, open:float, high:float, low:float, close:float, volume:int, wap:float, count:int):

super().realtimeBar(reqId, time, open, high, low, close, volume, wap, count)

print("RealTimeBars. ", reqId, ": time ", time, ", open: ",open, ", high: ", high, ", low: ", low, ", close: ", close, ", volume: ", volume,", wap: ", wap, ", count: ", count)

@iswrapper

def scannerParameters(self, xml:str):

open('scanner.xml', 'w').write(xml)

@iswrapper

def position(self, account: str, contract: ibapi.contract.Contract, position: float, avgCost: float):

print('Position: {} {} @ {}'.format(position, contract.symbol, avgCost))

@iswrapper

def positionEnd(self):

pass

def fundamentalData(self, reqId: TickerId, data: str):

print("FundamentalData. ", reqId, data)

def newsProviders(self, newsProviders: ListOfNewsProviders):

print("newsProviders: ")

for provider in newsProviders:

print(provider)

def historicalData(self, reqId:int, bar: BarData):

row = []

row.append(str(bar.date))

row.append(bar.open)

row.append(bar.high)

row.append(bar.low)

row.append(bar.close)

row.append(bar.volume)

row.append(bar.barCount)

row.append(bar.average)

self.hDataRecords.append(row)

self.hDataIndex.append(self.lineCount)

self.lineCount += 1

print("HistoricalData. ", reqId, " ,Date:", bar.date, ",Open:", bar.open,",High:", bar.high, ",Low:", bar.low, ",Close:", bar.close, ",Volume:", bar.volume,",Count:", bar.barCount, ",WAP:", bar.average)

def historicalDataEnd(self, reqId: int, start: str, end: str):

super().historicalDataEnd(reqId, start, end)

self.hData["columns"] = self.hDataColumns

self.hData["index"] = self.hDataIndex

self.hData["data"] = self.hDataRecords

#Format:

#jsonOut = {"columns":["Date","Open","High"],

#"index":[0, 1],

#"data": [["2017-12-18", 268.08, 268.67], ["2017-12-19", 268.48, 268.53]]}

if(self.currentSymbol == 'SPY'):

current_file = 'data/spy_current.json'

month_file = 'data/spy_month.json'

all_file = 'data/spy.json'

all_file_csv = 'data/spy.csv'

elif(self.currentSymbol == 'IWM'):

current_file = 'data/iwm_current.json'

month_file = 'data/iwm_month.json'

all_file = 'data/iwm.json'

all_file_csv = 'data/iwm.csv'

jsonDump = json.dumps(self.hData)

if(self.hDataCurrent):

#write the current file

with open(current_file, 'w') as f:

f.write(jsonDump)

self.hDataCurrent = False

elif(self.hDataMonthly):

with open(month_file, 'w') as f:

f.write(jsonDump)

self.hDataMonthly = False

else:

with open(all_file, 'w') as f:

#writer = csv.writer(f, delimiter=',', lineterminator='\r\n', quotechar="'")

f.write(jsonDump)

w = csv.writer(open(all_file_csv, "wt", newline=''), quoting=csv.QUOTE_NONE, escapechar=' ', quotechar='')

#w = csv.writer(fw, delimiter=',', lineterminator='\r\n', quotechar="'")

for item in self.hData.items():

w.writerow([item[1]])

#clear hData

self.hData.clear()

self.hDataRecords.clear()

self.hDataIndex.clear()

self.lineCount = 0

print("HistoricalDataEnd ", reqId, "from", start, "to", end)

if(self.isConnected()):

self.disconnect()

def historicalDataUpdate(self, reqId: int, bar: BarData):

print("HistoricalDataUpdate. ", reqId, " Date:", bar.date, "Open:", bar.open,"High:", bar.high, "Low:", bar.low, "Close:", bar.close, "Volume:", bar.volume,"Count:", bar.barCount, "WAP:", bar.average)

def main():

#put your calls in here

if __name__ == "__main__":

main()

Further Steps

Now we need to create some charts. Follow the example for momentum described in my previous blog post.